Global Markets

Geopolitical tensions between the U.S. and China escalated, following President Donald Trump’s threat to impose an additional 100% tariff on Chinese goods effective November 1, 2025. In response, China announced export restrictions on rare earth metals, intensifying fears of a renewed trade war. This pushed investors toward safe-haven assets, particularly U.S. Treasuries. Federal Reserve officials, including Christopher Waller and Mary Daly, signaled cautious support for further monetary easing while highlighting early signs of labor market softening.Indonesian Markets

Domestically, Indonesia’s local currency bond market strengthened as global risk sentiment improved and domestic liquidity remained abundant. Government bond yields declined across the curve, with the 10-year benchmark yield dropping 20–21 bps to around 6.09–6.12%, and the 5-year yield down 9 bps to 5.38%. The Jakarta Composite Index (JCI) rose 1.7% WoW to a record 8,258, led by conglomerate and commodity stocks. The Rupiah slightly weakened to IDR 16,570/USD, remaining broadly stable as Bank Indonesia was expected to provide liquidity support via open market operations.

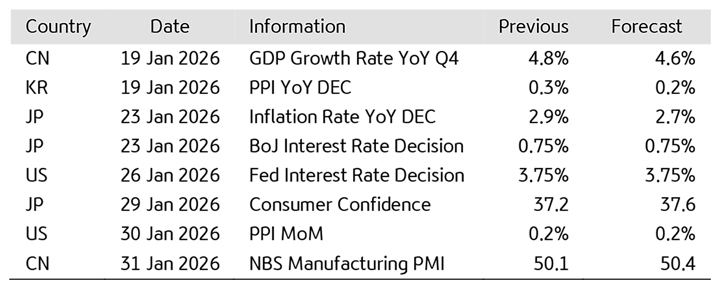

Weekly Highlight on Economic Indicators

Our Take:

The past week was dominated by renewed U.S.–China trade tensions, a prolonged U.S. government shutdown, and mounting expectations for Fed rate cuts, all of which drove a global bond rally. In Indonesia, stable domestic liquidity, robust auction demand, and controlled inflation helped sustain the bond market rally and maintain positive sentiment in equities, despite ongoing foreign outflows from the banking sector.The recommendation for investment to our investors (in order):

Fixed Income Fund > Equity Fund > Balanced Fund > Money Market Fund.

Author : KBVAM Investment Team

Source: Bloomberg, Infovesta, Trading Economics

DISCLAIMER :

INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.

This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

Latest Weekly Insight

Weekly Insight

Edge of Uncertainty

30 March 2026Weekly Insight

Edge of Uncertainty

30 March 2026

Global Markets

Global markets weakened amid high volatility due to the escalation of the U.S.–Iran conflict, against a backdrop of conflicting uncertainties surrounding peace negotiations. This drove a surge in oil prices, heightened expectations of inflation and higher for longer interest rates, and triggered risk-off sentiment and stagflation concerns. Looking ahead to next week, markets are expected to remain volatile with a downward bias, influenced by the progress of those negotiations, oil price movements, and key data (ISM, ADP, NFP), though there is potential for a temporary rally amid oversold conditions and thin liquidity ahead of Good Friday.

Indonesian Markets

Indonesia’s financial markets weakened last week amid consolidation driven by global risk-off sentiment (rising oil prices, high U.S. Treasury yields), pressure on the rupiah, and foreign capital outflows, although fundamentals remained stable. Next week, JCI is expected to see limited movement with a downward bias, with focus on inflation (risks from Ramadan and food/energy prices), the trade balance, and the manufacturing PMI; sentiment will remain bearish in the short term if inflation is high or the PMI weakens, which could put pressure on the rupiah and the JCI.

Weekly Highlight on Economic Indicators

Our Take:

JCI dropped -0.14% WoW to 7,097, with market capitalization down 0.24%, although liquidity remained solid and foreign investors continued to be net sellers. The market was dominated by consolidation, briefly strengthening on the back of the banking sector, but was held back by global pressures (a strong dollar, rising US yields) that triggered profit-taking and outflows. The energy sector held up amid rising commodity prices, while the lack of domestic catalysts made the market more sensitive to external factors.

Investment recommendations for our investors (in order of preference):

Fixed Income Fund > Money Market Fund > Balanced Fund > Equity Fund

Author : KBVAM Investment TeamSource: Bloomberg, Infovesta, Trading Economics

DISCLAIMER :INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

20260325-108.jpg)

Weekly Insight

Negative Bias Phase

25 March 2026Weekly Insight

Negative Bias Phase

25 March 2026

Global Markets

Global markets weakened amid escalating Middle East tensions after Trump threatened to destroy Iran’s energy facilities if the Strait of Hormuz was not opened, and Iran retaliated with threats against regional energy infrastructure driving up oil prices, inflation, and expectations of higher interest rates, which weighed on stocks and pushed up yields. This week, markets remain volatile and dependent on geopolitical developments and energy prices, with a focus on global PMI releases as the main catalyst, accompanied by other key data such as the UK CPI, U.S. durable goods orders, jobless claims, and consumer sentiment.

Indonesian Markets

Indonesia’s financial markets were volatile and trended lower due to global pressures stemming from the Middle East conflict, which triggered rising oil prices, capital outflows, and a weakening rupiah, amid limited trading and the Bank of Indonesia maintaining its hawkish stance at 4.75%. This week, the market remains shrouded in global uncertainty, so movements are expected to remain volatile with a greater risk of decline, although there is a chance of a rebound; therefore, the strategy remains defensive and selective.

Weekly Highlight on Economic Indicators

Our Take:

IHSG dropped -4.49% WoW to 7,106 amid low trading volume ahead of the long holiday, reflecting a consolidation phase with a negative bias. Market activity declined (volume -5.75%, frequency -15.28%), indicating a wait and see stance, but the surge in transaction value (+17.65%) suggests institutional dominance and rotation in large cap stocks. External pressures such as geopolitical escalation, rising oil prices, and a strengthening US dollar have led to defensive tendencies and increased interest in safe-haven assets.

Investment recommendations for our investors (in order of preference):

Fixed Income Fund > Money Market Fund > Balanced Fund > Equity Fund

Author : KBVAM Investment TeamSource: Bloomberg, Infovesta, Trading Economics

DISCLAIMER :INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

Weekly Insight

Holding The Line

02 March 2026Weekly Insight

Holding The Line

02 March 2026

Global Markets

Global markets were defensive this week, driven by a rotation from growth/AI to defensive sectors. Negative sentiment was triggered by high AI valuations, hot PPI, and US-Iran tensions. Yield UST 10Y fell to 3.9% due to increased safe haven demand, while non-US markets were more resilient (EAFE & EM rose), reflecting diversification away from US big tech. Next week, markets are expected to be volatile, focus will be on ISM PMI, JOLTS, Jobless Claims, ADP, and NFP, which will influence Fed rate expectations. The rotation toward defensive stocks, large-caps, bonds, and commodities continues, while aggressive leverage should be avoided.

Indonesian Markets

Indonesian market moved mixed and defensively, influenced by global and domestic sentiment. Stocks, bonds, and commodity markets showed moderate volatility. Foreign net selling increased, SBN yields were stable-to strong, especially for medium to long tenors. Next week, the market is expected to adopt a wait and see approach, focusing on rupiah stability, yield direction, foreign inflows, and global data affecting Fed interest rate expectations (NFP, ISM PMI) and domestic indicators such as the consumer confidence index and Q1 growth projections >5.39%, driven by improved labor absorption and seasonal consumption momentum ahead of Eid al-Fitr.

Weekly Highlight on Economic Indicators

Our Take:

JCI fell -0.44% to 8,235 from 8,271, with market capitalization down 1.03% due to foreign net selling pressure of Rp694 billion. The decline was triggered by negative sentiment surrounding geopolitical tensions in the Middle East, uncertainty over US tariffs, and warnings from S&P regarding Indonesia's fiscal risks. Despite the correction, trading activity increased significantly, with daily transaction values rising 25.35%. The JCI remained resilient despite facing global and domestic pressures, with dynamic trading.

Investment recommendations for our investors (in order of preference):

Equity Fund > Fixed Income Fund > Balanced Fund > Money Market Fund

Author : KBVAM Investment TeamSource: Bloomberg, Infovesta, Trading Economics

DISCLAIMER :INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

Weekly Insight

Correction Phase

26 January 2026Weekly Insight

Correction Phase

26 January 2026

Global MarketsGlobal markets are volatile with a cautious bias amid geopolitical risks. Pressure from US tariff issues eased as threats related to Greenland were lifted, supported by the US GDP for the third quarter of 2025 being revised upward from 4.3% to 4.4%, without inflationary pressure and improving global sentiment, encouraging limited risk-on sentiment. President Trump has added to political tensions by imposing new sanctions and hinting at potential military action against Iran. The Fed is expected to keep its benchmark interest rate at 3.5%-3.75%. Next week's focus will be on the FOMC, with market direction determined by Powell's tone on the timing of interest rate cuts in 2026 and the release of PPI and labor data that could trigger volatility.

Indonesian MarketsDomestic stock market recorded a decline, pressured by profit taking, a strengthening US dollar, and rising US Treasury yields, which triggered foreign outflows. In addition, the volatility of the rupiah and policy uncertainty following the revocation of PT Agincourt Resources' Martabe gold mining permit also affected market sentiment. Next week, the market is expected to consolidate, with investors awaiting the announcement of MSCI's free float calculation methodology (30/01) and monitoring domestic macro data and FY2025 banking-consumption financial reports, with external risks remaining dominant from the US Core PCE and the direction of Fed policy.

Weekly Highlight on Economic Indicators

Our Take:The JCI corrected 1.37% WoW to 8,951 from 9,075, with high volatility, despite briefly hitting an ATH of 9,134. Liquidity increased (ADV +9.32%; transaction value +3.59%), but market capitalization dropped 1.62% to IDR 16,244 trillion, reflecting dominant selling pressure. The decline was triggered by a net foreign sell of IDR 3.25 trillion, led by banking and mining; sectorally, the decline was led by Transportation & Logistics, Industrials, Energy, and Technology, signaling a correction phase with a cautious bias amid active investor distribution.

The recommendation for investment to our investors (in order):

Equity Fund > Fixed Income Fund > Balanced Fund > Money Market Fund.

Author : KBVAM Investment TeamSource: Bloomberg, Infovesta, Trading Economics

DISCLAIMER :INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

Latest Daily Market Wrap

Daily Market Wrap

March 31, 2026

31 March 2026Daily Market Wrap

March 31, 2026

31 March 2026NEWS

- America :

Wall Street was mixed (S&P 500 -0.39%, Nasdaq -0.73%, Dow +0.11%), pressured by the surge in oil prices due to escalating Middle East tensions, which dampened hopes for peace. Although negotiations are still ongoing, threats to Iran’s energy facilities persist, increasing inflation risks and weighing on technology stocks. Meanwhile, dovish comments from Powell eased interest rate concerns and triggered selective buying. The UST 10Y yield declined to 4.33% amid falling rate expectations and a shift toward safe-haven assets.

- Asia : Asian markets were mixed (Nikkei 225 -2.79%, KOSPI -2.97%, China SSE +0.24%, Hang Seng -0.81%) as the escalation of the US–Iran conflict heightened inflation risks and pressured growth, particularly for energy-importing countries. Selling was driven by geopolitical uncertainty and hawkish signals from the BOJ, with investors remaining defensive despite the emergence of limited buying interest.

MARKET UPDATE

-

The JCI closed slightly lower by -0.08% at 7,091, pressured by the escalation of the US–Iran conflict, which drove higher oil prices, rupiah depreciation, and foreign net selling. The financial sector declined (-1.17%), while the energy sector gained (+2.18%). Domestically, the market is monitoring fiscal efficiency measures (WFH & B50), the potential increase in non-subsidized fuel prices starting April 1, and uncertainty surrounding export duties on coal and nickel.

- Bond market: The 10-year government bond (SUN) yield declined to 6.83%, reflecting selective buying, particularly by domestic investors, amid Bank Indonesia’s decision to hold rates and ongoing global volatility. Despite external pressures (elevated UST yields, energy inflation, and outflows), the bond market remains relatively resilient, supported by strong local demand and limited inflows sustaining prices.

Source : Bloomberg, Infovesta --- DISCLAIMER : INVESTMENT IN MUTUAL FUNDS INVOLVES RISKS. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. BEFORE INVESTING, PLEASE CAREFULLY READ AND UNDERSTAND THE PROSPECTUS. This document was prepared by PT KB Valbury Asset Management based on information from reliable sources. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising from actions taken based on this document, whether suffered by any person or party.

Daily Market Wrap

March 30, 2026

30 March 2026Daily Market Wrap

March 30, 2026

30 March 2026NEWS

- America :

Wall Street declined (S&P 500 -1.67%, Nasdaq -2.15%, Dow -1.73%), driven by a repricing of risk assets following the escalation of the US–Iran conflict, which pushed oil prices higher and raised inflation expectations. Ongoing uncertainty around negotiations further reinforced risk-off sentiment. The US 10Y Treasury yield rose to 4.43%, pressuring valuations—particularly in the technology sector—amid weakening consumer sentiment.

-

Europe :

European markets weakened (STOXX 600 -0.9%) due to uncertainty surrounding the Middle East conflict and mixed signals regarding US–Iran negotiations. Investors struggled to interpret conflicting indications about the status of peace talks in the region.

- Asia : Asian markets were mixed (Nikkei 225 -0.43%, KOSPI -0.40%, China SSE +0.63%, Hang Seng +0.38%), driven by risk-off sentiment from Middle East tensions, rising oil prices, and concerns over inflation and higher interest rates. Japan and Korea declined, led by the technology sector, while China and Hong Kong gained, supported by industrial profit data.

MARKET UPDATE

-

The JCI declined -0.94% to 7,097, pressured by risk-off sentiment stemming from uncertainty in the US–Iran conflict, which pushed oil prices higher. The decline was exacerbated by foreign outflows, profit-taking, and negative sentiment surrounding coal export tariffs. Weakness was led by blue-chip banking and infrastructure stocks amid a lack of positive catalysts.

- Bond market: The 10Y Indonesian government bond (SUN) yield rose to 6.84%, with bond price pressure remaining orderly (no panic selling). The increase was driven by energy-related inflation risks and elevated US Treasury yields, leading to higher EM risk premiums and limited outflows—indicating that bonds have not fully acted as a safe haven amid “higher for longer” expectations.

Source : Bloomberg, Infovesta --- DISCLAIMER : INVESTMENT IN MUTUAL FUNDS INVOLVES RISKS. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. BEFORE INVESTING, PLEASE CAREFULLY READ AND UNDERSTAND THE PROSPECTUS. This document was prepared by PT KB Valbury Asset Management based on information from reliable sources. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising from actions taken based on this document, whether suffered by any person or party.

Daily Market Wrap

March 26, 2026

26 March 2026Daily Market Wrap

March 26, 2026

26 March 2026NEWS

- America :

The IHSG rose 2.75% to 7,302, driven by a post-holiday rebound and global risk-on sentiment from easing U.S.–Iran tensions, along with a rally in large-cap stocks. Despite the gains, the market remained rational and fundamentals-driven, while closely monitoring global negotiations, the dividend season, and domestic fiscal sentiment.

- Asia : The 10-year government bond (SUN) yield increased to 6.91%, reflecting selective selling pressure amid caution over persistently high global interest rates and rupiah weakness. Although the BI Rate remains stable and fiscal conditions are well maintained, investors continue to take a defensive stance, particularly on longer tenors.

MARKET UPDATE

-

The JCI declined 0.96% to 7,939, driven by the escalation of the US/Israel conflict with Iran, which triggered risk-off sentiment and a surge in oil prices. The pressure was further compounded by inflation at 4.76% YoY and foreign outflows, with deeper declines led by energy and mining stocks. Transaction value remained high at around IDR 29.8 trillion, reflecting dominant selling pressure, while the Financial Services Authority (OJK) remained on alert to maintain market stability and preserve investor confidence.

- Bond market: The 10-year Indonesian government bond (SUN) yield rose to 6.52%, driven by global risk-off sentiment following the escalation in the Middle East, which increased the risk premium for emerging markets. Pressure also came from domestic inflation, foreign outflows, and anticipation of policy decisions from the Fed and Bank Indonesia amid fiscal deficit concerns. Weak auction demand indicates that bond market sentiment remains cautious with elevated volatility.

Source : Bloomberg, Infovesta --- DISCLAIMER : INVESTMENT IN MUTUAL FUNDS INVOLVES RISKS. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. BEFORE INVESTING, PLEASE CAREFULLY READ AND UNDERSTAND THE PROSPECTUS. This document was prepared by PT KB Valbury Asset Management based on information from reliable sources. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising from actions taken based on this document, whether suffered by any person or party.

Daily Market Wrap

March 25, 2026

25 March 2026Daily Market Wrap

March 25, 2026

25 March 2026NEWS

- America :

The IHSG rose 1.20% to 7,106, driven by bargain hunting ahead of the holiday. However, the gains were limited and likely short-term amid global pressures (Middle East geopolitical tensions, rising energy prices, and market volatility). The surge in oil and gas prices has heightened inflation concerns. Last week, the Fed, ECB, BoE, and BoJ all kept interest rates unchanged.

- Asia : The 10-year Indonesian government bond (SUN) yield fell to 6.87% as selling pressure eased and buying interest emerged, supported by stabilizing U.S. Treasury yields and Bank Indonesia holding its policy rate at 4.75%. However, sentiment remains defensive due to external risks and foreign outflows, keeping movements relatively limited.

MARKET UPDATE

-

The JCI declined 0.96% to 7,939, driven by the escalation of the US/Israel conflict with Iran, which triggered risk-off sentiment and a surge in oil prices. The pressure was further compounded by inflation at 4.76% YoY and foreign outflows, with deeper declines led by energy and mining stocks. Transaction value remained high at around IDR 29.8 trillion, reflecting dominant selling pressure, while the Financial Services Authority (OJK) remained on alert to maintain market stability and preserve investor confidence.

- Bond market: The 10-year Indonesian government bond (SUN) yield rose to 6.52%, driven by global risk-off sentiment following the escalation in the Middle East, which increased the risk premium for emerging markets. Pressure also came from domestic inflation, foreign outflows, and anticipation of policy decisions from the Fed and Bank Indonesia amid fiscal deficit concerns. Weak auction demand indicates that bond market sentiment remains cautious with elevated volatility.

Source : Bloomberg, Infovesta --- DISCLAIMER : INVESTMENT IN MUTUAL FUNDS INVOLVES RISKS. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. BEFORE INVESTING, PLEASE CAREFULLY READ AND UNDERSTAND THE PROSPECTUS. This document was prepared by PT KB Valbury Asset Management based on information from reliable sources. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising from actions taken based on this document, whether suffered by any person or party.

Latest Publication

Publication

Valbury Money Market I Emerges As Champion

26 February 2026Publication

Valbury Money Market I Emerges As Champion

26 February 2026-All_KBValburyAM-61.jpg "Image: https://kbvalburyasset.co.id/images/news/PiagamBMFA26(A4)-All_KBValburyAM-61.jpg") PT

KB Valbury Asset Management has once again received recognition for its

outstanding performance as an Investment Manager by winning an award at the

Best Mutual Fund Awards 2026. The event was held on Wednesday, February 25,

2026, at Hotel Habitate, Jakarta.

At the

event, the Valbury Money Market I Mutual Fund successfully won an award in the

5-Year Money Market Fund Category for funds with assets ranging from IDR 10

billion to IDR 100 billion. This award serves as proof of the fund’s consistent

performance and its disciplined, well-measured investment management strategy

over the past five years.

PT

KB Valbury Asset Management has once again received recognition for its

outstanding performance as an Investment Manager by winning an award at the

Best Mutual Fund Awards 2026. The event was held on Wednesday, February 25,

2026, at Hotel Habitate, Jakarta.

At the

event, the Valbury Money Market I Mutual Fund successfully won an award in the

5-Year Money Market Fund Category for funds with assets ranging from IDR 10

billion to IDR 100 billion. This award serves as proof of the fund’s consistent

performance and its disciplined, well-measured investment management strategy

over the past five years.

Publication

Promotion

23 December 2025Publication

Promotion

23 December 2025Promotion Terms & Conditions :

- Minimum purchase of KB Valbury Asset Management Mutual Fund equivalent to IDR 1,000,000 will get a Bonus of IDR 100,000 if the participants meet all the terms and conditions of the program.

- Valid for Valbury Prime Dynamic Equity Mutual Fund products.

- Purchases of Mutual Funds for this promotion program can only be made on January 5-9, 2026 and must be through BRAVO.

- Participants who do not make redemption transactions during the program period (5-30 January 2026) will get a maximum participation unit bonus of Rp. 100,000 (One Hundred Thousand Rupiah).

- Participants who make redemption transactions during the program period (5-30 January 2026) are considered to have failed and are not entitled to bonuses.

- The promotion is valid for the first 100 customers (new customers with no investment history)

- The promotion is not valid for KB Valbury Asset Management’s employees.

- The bonus is in the form of Valbury Prime Dynamic Equity mutual fund participation units.

- The bonus will be given, no later than 7 working days after the end of the promotion program.

- Taxes on the bonus received by the customer are borne by the Prize Recipient in accordance with applicable tax provisions.

- This promotion cannot be combined with other promotions.

General Conditions :

- Prizes are non-transferable.

- The decision of PT KB Valbury Asset Management in determining the winner is absolute and cannot be contested.

- KBVAM reserves the right to disqualify and cancel any bonus if there are indications of abuse of any form by participants and/or violations of terms and conditions.

- KBVAM may change or terminate the promo and it’s terms and conditions at any time without prior notice.

- This policy is effective from 5 January 2026 and if there are any changes it will be further confirmed.

- Provisions that have not been listed in this circular letter (if any) will be regulated later.

Publication

PLAN OF AMENDMENT KIK & PROSPECTUS OF MUTUAL FUND KBVAM

01 December 2025Publication

PLAN OF AMENDMENT KIK & PROSPECTUS OF MUTUAL FUND KBVAM

01 December 2025ANNOUNCEMENT OF PLANNING TO CHANGE COLLECTIVE INVESTMENT CONTRACTS ("KIK") AND PROSPECTUS OF MUTUAL FUNDS MANAGED BY PT KB VALBURY ASSET MANAGEMENT

PT KB Valbury Asset Management, as Investment Manager of:

- VALBURY STABLE GROWTH FUND;

- VALBURY INVESTASI BERIMBANG FUND;

- VALBURY LIQUID FUND;

- VALBURY MONEY MARKET I FUND; and

- VALBURY PRIME DYNAMIC EQUITY FUND.

intends to announce planned changes to the Investment Cooperative Investment Fund (KIK) and Prospectus of KB VALBURY MUTUAL FUNDS, with the following details :

I. Planned changes to the Investment Cooperative Investment Fund (KIK) and Prospectus of KB VALBURY MUTUAL FUNDS

- Change of the Investment Manager's name from "PT Valbury Capital Management" to "PT KB Valbury Asset Management";

- Change of the name of KB VALBURY MUTUAL FUNDS in connection with the change of the Investment Manager's name as referred to in point 1) above;

- Additional information on the Auto-debit mechanism for periodic payments for Participation Unit purchases of KB VALBURY MUTUAL FUNDS by KB VALBURY MUTUAL FUNDS Unit Holders.

- Additional payment methods for purchasing Participation Units in VALBURY MUTUAL FUNDS by Unit Holders can be made through a Virtual Account;

- Additional information that payment for purchasing Participation Units in VALBURY MUTUAL FUNDS into VALBURY MUTUAL FUNDS accounts can be made by transfer via electronic means, including payment gateways and QRIS (Quick Response Code Indonesian Standard), as long as it complies with applicable laws and regulations;

- Updated correspondence addresses for the Investment Manager for all VALBURY MUTUAL FUNDS, except for the VALBURY LIQUID FUND.

- Changes to the Composition of the Board of Directors and Investment Management Team of the Investment Manager; and

- Adjustments to the provisions in the KIK and Prospectus to the Laws and Regulations of the Financial Services Authority ("POJK"), including the following:

- Law Number 4 of 2023, dated January 12, 2023, concerning the Development and Strengthening of the Financial Sector;

- OJK Regulation Number 17/POJK.04/2022, dated September 1, 2022, concerning the Guidelines for Investment Manager Conduct;

- OJK Regulation Number 4 of 2023, dated March 30, 2023, concerning the Second Amendment to OJK Regulation 23/POJK.04/2016 concerning Mutual Funds in the Form of Collective Investment Contracts;

- OJK Regulation Number 8 of 2023, dated June 14, 2023, concerning the Implementation of Anti-Money Laundering, Counter-Terrorism Financing, and Counter-Proliferation of Weapons of Mass Destruction Programs in the Financial Services Sector;

- OJK Regulation Number 22 of 2023, dated December 22, 2023, concerning OJK Regulation Concerning Consumer and Community Protection in the Financial Services Sector;

- OJK Regulation Number 22/POJK.04/2017 dated June 21, 2017, concerning Securities Transaction Reporting; and

- OJK Regulation Number 33 of 2024 dated December 19, 2024, concerning the Development and Strengthening of Investment Management in the Capital Market;

- OJK Regulation Number 56/POJK.04/2020 dated December 3, 2020, concerning Mutual Fund Reporting and Accounting Guidelines (specifically for VALBURY INVESTMENT BALANCED MUTUAL FUNDS and VALBURY MONEY MARKET I MUTUAL FUNDS);

- OJK Regulation Number 31/POJK.07/2020 dated April 22, 2020, concerning the Provision of Consumer and Public Services in the Financial Services Sector by the Financial Services Authority (specifically for VALBURY INVESTMENT BALANCED MUTUAL FUNDS and VALBURY MONEY MARKET I MUTUAL FUNDS);

- OJK Regulation Number 18/POJK.07/2018 dated September 10, 2018 concerning Consumer Complaints Services in the Financial Services Sector (specifically for VALBURY INVESTMENT BALANCED MUTUAL FUNDS and VALBURY MONEY MARKET I MUTUAL FUNDS); and

- OJK Regulation Number 61/POJK.07/2020 dated December 14, 2020 concerning Alternative Dispute Resolution Institutions in the Financial Services Sector (specifically for VALBURY INVESTMENT BALANCED MUTUAL FUNDS and VALBURY MONEY MARKET I MUTUAL FUNDS).

Publication

Resolving Investment Disputes in the Right Way: Getting to Know LAPS SJK

04 November 2025Publication

Resolving Investment Disputes in the Right Way: Getting to Know LAPS SJK

04 November 2025As part of our commitment to transparency and investor protection, we support dispute resolution mechanisms through the Financial Services Sector Alternative Dispute Resolution Institution (LAPS SJK).

LAPS SJK is an independent institution licensed and supervised by the Financial Services Authority (OJK), which functions to assist in the fair, swift, and out-of-court resolution of disputes between consumers and financial service providers—including investment management companies.

The existence of LAPS SJK is regulated in OJK Regulation (POJK) Number 61/POJK.07/2020 concerning the Alternative Dispute Resolution Institution for the Financial Services Sector, which forms the legal basis for the implementation of non-litigation dispute resolution processes in the financial services industry.

Services Provided

- Mediation: dispute resolution by facilitating dialogue between disputing parties to reach a mutually beneficial agreement through a negotiation process between the disputing parties.

- Arbitration: resolution of civil disputes through an arbitrator's decision outside of the general court system based on an Arbitration Agreement made in writing by the disputing parties.

- Binding Opinions: Provision of professional views on differences in interpretation in the implementation of agreements, for example regarding: interpretation of unclear provisions; additions or changes to provisions related to the emergence of new circumstances; or regarding certain legal relationships of an agreement.

Through LAPS SJK, customers have an easily accessible and reliable dispute resolution channel, while companies can maintain their integrity, professionalism, and investor confidence.

For more information, visit the official website www.lapssjk.id.

Source : http://www.lapssjk.id