Global Market Updates

The inflation rate in the US fell for 3 consecutive months to 3.0% YoY in June 2024, the lowest level since June 2023, lower than 3.3% YoY in May 2024 and below the consensus estimate of 3.1% YoY due to lower energy prices. The data encouraged an increase in investor expectations for US interest rate cuts and pressure on the USD Index, as well as a decline in US Treasury yields. (CNBC)

Asian Markets

The Chins headline inflation rate narrowed to 0.2% YoY in June 2024 from 0.3% YoY over the previous two months, lower than the consensus estimate of 0.4% YoY. Food prices fell by -2.1% YoY amid a fragile economic recovery, despite a sharp increase in pork prices during the Dragon Boat Festival. (Reuters)

China's trade surplus rose to USD99.05 billion in June 2024 from USD69.80 billion in May 2024, exceeding consensus expectations of USD85 billion. This is the largest trade surplus since July 2022 as exports grew by 8.6% YoY while imports fell by 2.3% YoY. (CNBC)

Indonesian Markets

Indonesia's consumer confidence index fell to 123.3 in June 2024 from 125.2 in May 2024, which is its lowest level since February 2024. Several sub-indices declined, namely economic outlook, income expectations, and job availability. (Reuters)

Weekly Highlight

This week, there will be domestic economic data releases for the balance of trade and the BI Governor's meeting decision. Globally, there will be economic information releases such as GDP growth from China, inflation rate from the UK, interest rate from the ECB, balance of trade, and inflation rate from Japan.

Our Take:

Global markets again showed divergent trends in 2Q24, with equities and gold making positive gains while bond returns were mixed. Equities was buoyed by resilient economic activity and a brighter corporate earnings outlook. Domestic earning growth expectations have been revised down post 1Q24 result but still decent at <9% for FY24F. Although there are some risks including Indonesia transition to new government as well as US election, therefore, we expect 2H outlook to be relatively steady vs 1H. At the June review and subsequent public remarks, Governor Warjiyo had suggested that the window to lower rates might open in 4Q24. We are mindful that the window for cuts hinges on the prevailing FX risks this quarter and the next. The incoming government’s fiscal bent and key cabinet appointees, especially for the finance portfolio, will also be matters of great interest.

As we did change (in our previous weekly update) our view for investor investment are (in order): Fixed Income Fund > Balanced Fund > Equity Fund > Money Market Fund

Author : KBVAM Investment Team

DISCLAIMER :

INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.

This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

Latest Weekly Insight

Weekly Insight

Trade Tension

14 May 2025Weekly Insight

Trade Tension

14 May 2025

Global MarketsFollowing two days of high-stakes talks in Switzerland, trade negotiators from the world’s biggest economies announced a significant tariff deescalation on Monday. In a carefully coordinated joint statement, the US reduced duties on Chinese products to 30% from 145% for 90 days, while Beijing lowered its levy on most goods to 10%.

This easing of US-China trade tensions offers investors the clearest signal yet that the Trump administration is adopting a softer stance after recent market-disrupting clashes. Consequently, with increased optimism that the US economy can avoid a recession, traders now anticipate only two Federal Reserve rate cuts in 2025.

Indonesian MarketsIndonesia's Q1 GDP grew by 4.87% YoY, according to BPS, falling short of the 4.92% economists' expectation. Contributing factors included a 4.89% YoY expansion in private consumption, a 1.38% YoY contraction in government spending, a 2.12% YoY increase in gross fixed capital formation, and a substantial 6.78% YoY growth in exports.

The JCI maintained its upward trend, albeit at a slower pace, with a 0.25% increase. Meanwhile, the yield on the 10-year government bond decreased to 6.83%, and the rupiah showed limited movement at 16,532 against the US dollar.

Weekly Highlight on Economic Indicators

Our Take:Our funds continue to show positive performance. Valbury Prime Dynamic Equity recorded a gain of 0.47% (BM: 0.65%), Valbury Investasi Berimbang rose by 1.17% (BM: 0.32%), and Valbury Stable Growth Fund increased by 0.35% (BM: 0.18%).

The moderation of trade tensions, which should lessen imported inflationary pressures, coupled with Indonesia's weaker-than-anticipated GDP growth, makes it more probable that Bank Indonesia will consider an interest rate cut at its upcoming meeting this month.

The recommendation for investment to our investors (in order) :

Money Market Fund > Fixed Income Fund > Balanced Fund > Equity Fund.

Author : KBVAM Investment TeamSource: Bloomberg, Infovesta, Trading Economics

DISCLAIMER :INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

Weekly Insight

Consistent With Expectations

25 February 2025Weekly Insight

Consistent With Expectations

25 February 2025

Global MarketsEuropean equity funds experienced their most substantial weekly inflows in three years, with approximately $4 billion in capital entering the region through February 19th. This figure, the highest since February 2022, also confirms a second consecutive week of net inflows into European equities.

BofA strategist Michael Hartnett reiterated his preference for global stocks over US equities, citing improved business activity and the relative attractiveness of markets like Germany, China, Japan, and South Korea. He also cautioned that US markets face the risk of an unexpected economic slowdown. Amid a flight to safety, traders fueled a prolonged rally in US Treasuries, resulting in the US 10-year note yield dropping to 4.43%.

Indonesian MarketsBank Indonesia maintained its benchmark interest rate at 5.75% to stabilize the rupiah amidst global uncertainty and reduced expectations of Federal Reserve rate cuts. While noting potential for rate reductions due to low domestic inflation, the central bank opted for stability. This week, the 10-year government bond yield slightly increased to 6.79%, while the rupiah remained stable around 16,300 per US dollar. The broader stock market (JCI) saw a 2.48% gain, though the LQ45 index rose by a more modest 0.56%.

Weekly Highlight on Economic Indicators

Our Take:While stock and bond markets saw positive returns this week, our funds demonstrated outperformance relative to their peers. Valbury Prime Dynamic Equity rose by 1.42% (BM: 0.91%), Valbury Investasi Berimbang improved by 1.72% (BM: 0.52%), Valbury Stable Growth Fund gained 0.54% (BM: 0.22%) and Valbury Money Market I increased by 0.10% (BM: 0.10%).

Consistent with expectations, Bank Indonesia, maintained its interest rate, signaling caution amidst global uncertainty. This week's release of the Fed's preferred inflation gauge will provide investors with potential insights into the Fed's policy direction.

The recommendation for investment to our investors (in order) :

Fixed Income Fund > Money Market Fund > Balanced Fund > Equity Fund.

Author : KBVAM Investment Team

DISCLAIMER :INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

Weekly Insight

Rupiah Holds Steady

18 February 2025Weekly Insight

Rupiah Holds Steady

18 February 2025

Global MarketsJanuary's 0.9% drop in US retail sales—the steepest in nearly two years— signals a consumer spending pullback after late 2024's surge. This reignites Fed rate cut hopes despite strong inflation data. The bond market reacted positively to the news, closing the week with substantial gains. Meanwhile, the S&P 500 remained near its record highs, and the dollar weakened, reaching a new low for 2025.

DeepSeek's AI advancements are contributing to a shift in investment flows, with stock funds returning to China from India. This resurgence is reflected in a combined market capitalization increase of over $1.3 trillion for Chinese onshore and offshore equities in the past month, contrasting sharply with a more than $720 billion decline in India's market value. Specifically, the China SSE rose 1.30%, and the Hong Kong HSI saw a substantial 7.04% gain.

Indonesian MarketsIndonesia's capital market showed mixed results again last week. The Jakarta Composite Index (JCI) continued its decline, falling 1.54%, while the 10-year government bond yield dropped significantly to 6.74%.

Prabowo announced that Danantara will start operations this month. The sovereign wealth fund will invest in sustainable, high-impact projects across various sectors, with the goal of contributing to the country's 8% economic growth target. However, experts have raised concerns regarding the fund's strategy, governance, and its ability to achieve this ambitious objective.

Weekly Highlight on Economic Indicators

Our Take:Our fixed income fund capitalized on the bond market rally with continued strong performance. Besides, despite the stock market downturn, our equity and balanced funds outperformed the market.

Valbury Prime Dynamic Equity declined by 0.32% (BM: -0.54%), Valbury Investasi Berimbang improved by 0.09% (BM: -0.06%), Valbury Stable Growth Fund gained 0.40 (BM: 0.33%) and Valbury Money Market I increased by 0.10% (BM: 0.09%). Softer recent U.S. economic data is providing support for a more stable rupiah and potentially giving Bank Indonesia (BI) room for future rate cuts. However, we expect BI to hold rates steady at this week's meeting.

The recommendation for investment to our investors (in order) :

Fixed Income Fund > Money Market Fund > Balanced Fund > Equity Fund.

Author : KBVAM Investment Team

DISCLAIMER :INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

Weekly Insight

Low Inflation

11 February 2025Weekly Insight

Low Inflation

11 February 2025

Global MarketsUS President, Donald Trump, announced plans to unveil reciprocal tariffs last week, escalating the ongoing trade war and further fueling inflation fears, wiping out the week’s gain in the US stock market. The S&P 500 fell 0.95% on Friday and closed the week down 0.24%. US economic data revealed weakening consumer sentiment amid inflation worries, while mixed jobs figures pointed to a moderating but still healthy labor market, with notable wage growth. This strengthens the Federal Reserve's position that it is in no hurry to lower borrowing costs.

Indonesian MarketsIndonesia's capital market diverged last week, with investors shifting from stocks to bonds. This shift was likely influenced by the recent inflation report, which showed a YoY rate of 0.76%, significantly below consensus forecasts.

The Jakarta Composite Index (JCI) plummeted 5.16%, led by a significant 14.52% drop in Bank Mandiri (BMRI) shares. This decline followed a JP Morgan report that underweight the bank. During the week, foreign investors withdrew US$231.1 million from the stock market (as of Feb 7th), while bond inflows reached US$371.7 million (as of Feb 6th).

Notably, global funds purchased a net US$581.3 million in Indonesian

bonds on Feb 6th, the largest single-day purchase since Sept 19th. Consequently, the 10-year government bond yield dropped to 6.89%, while the JISDOR remained relatively stable at around 16,300 per US dollar.

Weekly Highlight on Economic Indicators

Our Take:The stock market's significant downturn led to losses in our equity and balanced funds. But, our fixed income fund benefited on the bond market rally, exceeding the performance of comparable funds.

Valbury Prime Dynamic Equity decreased by 3.98% (BM: -3.14%), Valbury Investasi Berimbang decreased by 3.71% (BM: -1.34%). On the other hand, Valbury Stable Growth Fund increased by 0.98% (BM: 0.52%) and Valbury Money Market I increased by 0.10% (BM: 0.10%).

Low inflation contributed to Bank Indonesia's (BI) surprise interest rate reduction last month. While this week's data may offer some insights, the direction of BI's policy at next week's meeting remains uncertain.

The recommendation for investment to our investors (in order) :

Fixed Income Fund > Money Market Fund > Balanced Fund > Equity Fund.

Author : KBVAM Investment Team

DISCLAIMER :INVESTMENT THROUGH MUTUAL FUNDS CONTAINS RISKS. PROSPECTIVE INVESTORS MUST READ AND UNDERSTAND THE PROSPECTUS BEFORE DECIDING TO INVEST THROUGH MUTUAL FUNDS. PAST PERFORMANCE DOES NOT REFLECT FUTURE PERFORMANCE.This document was prepared based on information from reliable sources by PT KB Valbury Asset Management. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising, whether against or suffered by any person or party and in any way deemed to be a result of actions taken on the basis of all or part of this document.

Latest Daily Market Wrap

Daily Market Wrap

December 20, 2024

20 December 2024Daily Market Wrap

December 20, 2024

20 December 2024NEWS

- The Bank of Japan kept its benchmark interest rate at 0.25% and the Bank of England also held its benchmark interest rate at 4.75%.

- Japan's core CPI in November recorded an increase of 2.7% YoY, above the estimate of 2.6%.

- Jobless claims in the United States based on the publication of December 14 were recorded at 220 thousand, below the estimate of 230 thousand.

MARKET UPDATE

- Indonesian stock market weakened with JCI declining by 1.84%.

- The biggest contributors: BYAN (1.50%), AMMN (1.13%), PGEO (7.22%)

- Biggest weakening contribution: BMRI (-2.58%), TPIA (-3.62%), BBCA (-1.28%)

- Indonesian bond market weakened with ICBI declining by 0.05%.

- The 10-year government bond yield rose to 7.08% from 7.07%.

- Rupiah exchange rate against US dollar weakened to IDR16,277/USD from IDR16,100/USD.

- Indonesia's 5-year CDS rose to 77.27 from 75.47.

Source : Bloomberg, Infovesta --- DISCLAIMER : INVESTMENT IN MUTUAL FUNDS INVOLVES RISKS. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. BEFORE INVESTING, PLEASE CAREFULLY READ AND UNDERSTAND THE PROSPECTUS. This document was prepared by PT KB Valbury Asset Management based on information from reliable sources. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising from actions taken based on this document, whether suffered by any person or party.

Daily Market Wrap

December 19, 2024

19 December 2024Daily Market Wrap

December 19, 2024

19 December 2024NEWS

- Bank Indonesia decided to maintain interest rates at 6.00% with a focus on strengthening the stability of the Rupiah exchange rate. (Bank Indonesia)

- The Fed cut its benchmark interest rate by 25bps with a target range of 4.25%-4.50%.

- Dollar index jumped significantly to the highest level since November 2022 after the Fed announcement.

MARKET UPDATE

- The Indonesian stock market weakened with the JCI declining by 0.70%.

- The biggest contributors: BREN (1.99%), ADRO (3.19%), CUAN (3.95%)

- Biggest weakening contribution: BMRI (-2.10%), BYAN (-2.32%), BBCA (-1.01%)

- Indonesian bond market weakened with ICBI declining by 0.03%.

- The 10-year government bond yield rose to 7.07% from 7.06%.

- Rupiah exchange rate against US dollar weakened to IDR16,100/USD from IDR16,050/USD.

- Indonesia's 5-year CDS rose to 75.47 from 73.72.

Source : Bloomberg, Infovesta --- DISCLAIMER : INVESTMENT IN MUTUAL FUNDS INVOLVES RISKS. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. BEFORE INVESTING, PLEASE CAREFULLY READ AND UNDERSTAND THE PROSPECTUS. This document was prepared by PT KB Valbury Asset Management based on information from reliable sources. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising from actions taken based on this document, whether suffered by any person or party.

Daily Market Wrap

December 18, 2024

18 December 2024Daily Market Wrap

December 18, 2024

18 December 2024NEWS

- Japan's November exports recorded an increase of 3.8% YoY, above the estimate of 2.5%.

- November US Retail Sales recorded an increase of 0.7% MoM, above the estimate of 0.6%.

- US Industrial Production in November recorded a decline of 0.1% MoM, below estimates of a 0.3% increase.

MARKET UPDATE

- Indonesian stock market weakened with JCI declining by 1.39%.

- The biggest contributors: BREN (4.45%), DSSA (1.89%), CUAN (1.88%)

- Biggest weakening contribution: BBRI (-2.35%), BBCA (-1.98%), BMRI (-2.06%)

- Indonesian bond market weakened with ICBI declining by 0.06%.

- The 10-year government bond yield fell to 7.06% from 7.07%.

- The Rupiah exchange rate against the US dollar weakened to IDR16,050/USD from IDR16,019/USD.

- Indonesia's 5-year CDS fell slightly to 73.72 from 73.77.

Source : Bloomberg, Infovesta --- DISCLAIMER : INVESTMENT IN MUTUAL FUNDS INVOLVES RISKS. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. BEFORE INVESTING, PLEASE CAREFULLY READ AND UNDERSTAND THE PROSPECTUS. This document was prepared by PT KB Valbury Asset Management based on information from reliable sources. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising from actions taken based on this document, whether suffered by any person or party.

Daily Market Wrap

November 29, 2024

29 November 2024Daily Market Wrap

November 29, 2024

29 November 2024NEWS

- The government agreed to reduce airfares for domestic flights by 10% over the Christmas and New Year period.

- Japan's industrial output increased by 3.0%, below the estimate of 4.0%.

- Bond sales in Europe reached €1.705 trillion, breaking the annual record.

MARKET UPDATE

- Indonesian stock market weakened with JCI declining by 0.63%.

- The largest weakening contributors: ADRO (-24.80%), BBRI (-1.59%), TPIA (-2.44%)

- Biggest supporting contribution: AMMN (1.65%), BMRI (0.78%), BBNI (1.52%)

- The Indonesian bond market rallied with an increase in ICBI by 0.11%.

- The 10-year government bond yield fell to 6.90% from 6.92%.

- The Rupiah exchange rate against the US dollar strengthened to IDR 15,864/USD from IDR 15,930/USD.

- Indonesia's 5-year CDS fell to 75.28 from 75.34.

Source : Bloomberg, Infovesta --- DISCLAIMER : INVESTMENT IN MUTUAL FUNDS INVOLVES RISKS. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. BEFORE INVESTING, PLEASE CAREFULLY READ AND UNDERSTAND THE PROSPECTUS. This document was prepared by PT KB Valbury Asset Management based on information from reliable sources. PT KB Valbury Asset Management does not guarantee the accuracy, adequacy or completeness of the information and materials provided. PT KB Valbury Asset Management Indonesia is not responsible for any legal and financial consequences arising from actions taken based on this document, whether suffered by any person or party.

Latest Publication

Publication

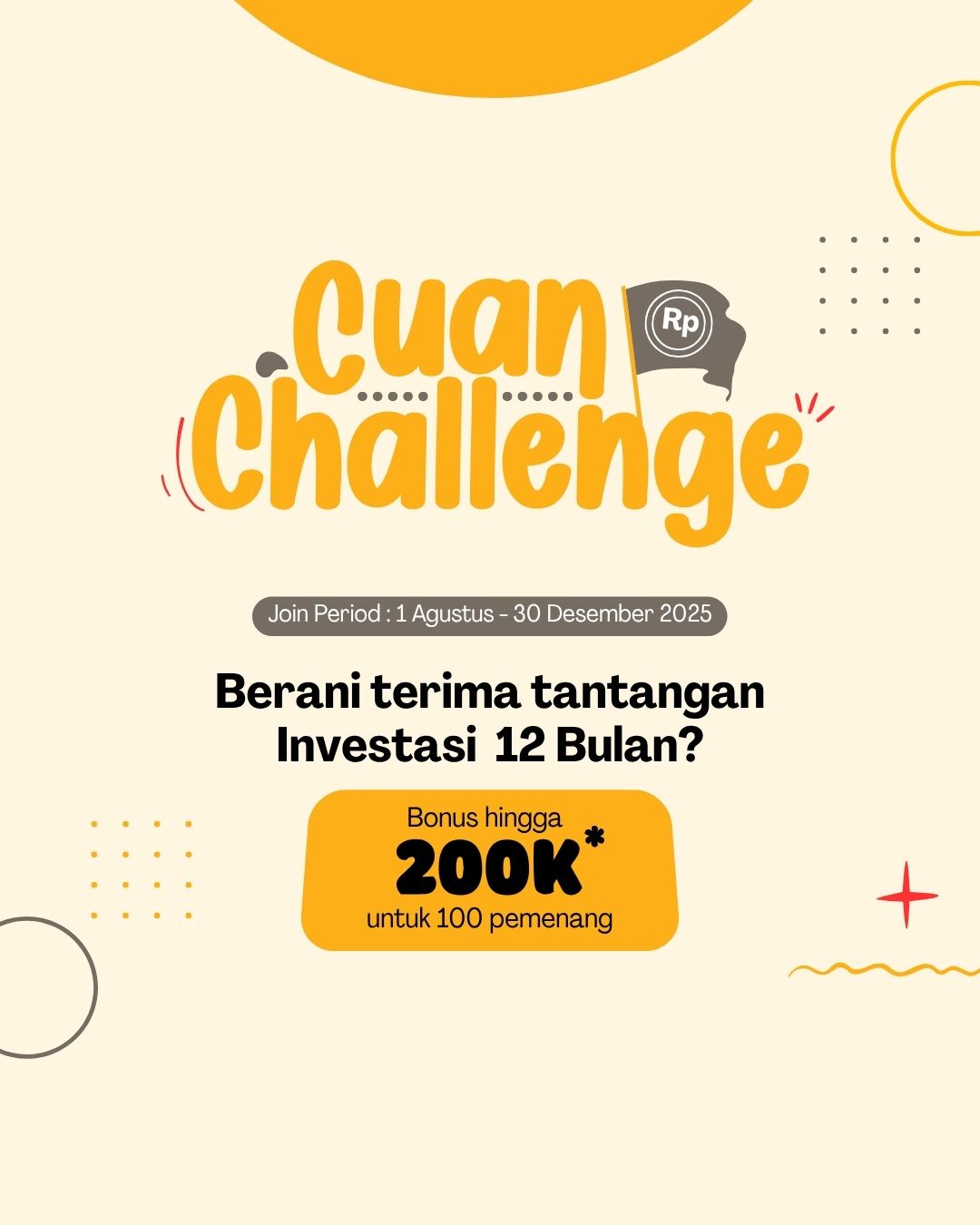

Cuan Challenge

09 July 2025Publication

Cuan Challenge

09 July 2025Program Terms & Conditions:

- Promotion applies to new, existing and KB group employees

- Customers who wish to participate in the CUAN CHALLENGE program are required to register in advance through the link available: bit.ly/joincuanchallenge

- For those who are interested in participating in the CUAN CHALLENGE program but are not yet KB Valbury Asset Management customers, they can open a mutual fund account online through BRAVO (https://bravo.valbury.co.id) or manually fill out a mutual fund account opening form before registering as a CUAN CHALLENGE program participant.

- Participants who have registered must make a subscription every month consecutively for 12 months, starting from the month when registering a minimum of Rp, 500,000, - (five hundred thousand rupiah).

- Products that are included in the CUAN CHALLENGE program are Mutual Fund Products: Valbury Money Market I

- Participants who do not make a subscription in 1 month or more during the regular investment period, will be disqualified.

- Participants who do not make redemptions and successfully complete the Cuan Challenge program for 12 months will get a participation unit bonus of Rp. 150,000 (one hundred and fifty thousand rupiah).

- The bonus will be given after each participant's periodic investment program ends in the form of mutual fund participation units (maximum 14 working days).

- Taxes on bonuses received by customers are borne by KB Valbury Asset Management in accordance with applicable tax regulations.

- Participants who have completed the Cuan Challenge program and have not made redemptions in the following 3 months will get an additional bonus of Rp.50,000 (fifty thousand rupiah).

- Prizes are non-transferable

- The decision of PT KB Valbury Asset Management (KBVAM) in determining the winner is absolute and cannot be contested.

- KBVAM has the right to disqualify and cancel the bonus if there are indications of misuse by participants and / or violations of the terms and conditions.

- KBVAM may change or terminate the promo and terms and conditions at any time without prior notice.

- This policy is effective as of August 01, 2025 and if there are any changes will be informed further.

- Provisions that have not been listed in this circular will be regulated later.

Publication

Having Fund with Telkom University by MNC Securities & KB Valbury AM

02 November 2024Publication

Having Fund with Telkom University by MNC Securities & KB Valbury AM

02 November 2024MNC Sekuritas dan KB Valbury AM Gandeng Mahasiswa Universitas Telkom Belajar Investasi Reksa Dana

BANDUNG, iNews.id - MNC Sekuritas merupakan perusahaan sekuritas yang aktif dan konsisten dalam menggelar kegiatan edukasi pasar modal untuk menciptakan investor yang berkualitas.

Salah satu bukti komitmen pengembangan investor pasar modal Tanah Air adalah konsistensi Perseroan dalam melakukan edukasi pasar modal, termasuk dalam rangka Bulan Inklusi Keuangan (BIK) dan Gerakan Nasional Cerdas Keuangan (GENCARKAN) MNC Sekuritas bersama KB Valbury Asset Management kembali berkolaborasi dalam menggelar edukasi reksa dana dalam rangkaian acara Having Fund 2024.

Kali ini edukasi dilaksanakan di Telkom University, Bandung pada Kamis (13/10/2024). Pemaparan materi disampaikan oleh General Manager KB Valbury Asset Management Dede Surjadi dan Senior Marketing Mutual Fund MNC Sekuritas Wesly Andri.

General Manager KB Valbury Asset Management Dede Surjadi mengatakan bahwa saat ini para mahasiswa ataupun karyawan yang baru mulai bekerja, harus mengenal dan paham mengenai investasi.

Hal ini diperlukan agar daya beli yang dimiliki tidak tergerus oleh inflasi dengan adanya imbal hasil yang optimal dengan risiko yang terukur.

“Untuk jangka panjang, pemahaman investasi sangat diperlukan untuk mempersiapkan kebebasan finansial bagi setiap individu di masa depan,” ujar Dede.

Wakil Dekan I Bidang Akademik Fakultas Ekonomi dan Bisnis Telkom University Deannes Isynuwardhana, PhD dalam keterangannya menyampaikan bahwa mahasiswa dan mahasiswi perlu untuk diberikan literasi dan informasi mengenai pasar modal.

“Harapannya kami ingin kegiatan seperti ini terus berlanjut sehingga mahasiswa-mahasiswi dapat memahami seperti apa pentingnya pasar modal,” tutur dia.

Nikmati layanan investasi saham dan reksa dana dari #MNCSekuritas dengan segera unduh aplikasi MotionTrade dan jelajahi seamless experience.

Aplikasi MotionTrade dapat diunduh di Google PlayStore dan Apple AppStore dengan link unduh onelink.to/motiontrade. MNC Sekuritas, Invest with The Best!

Editor: Puti Aini Yasmin

---

Artikel ini telah diterbitkan di halaman inews.id pada Sabtu, 02 November 2024 - 11:44:00 WIB oleh Tim iNews.id dengan judul "MNC Sekuritas dan KB Valbury AM Gandeng Mahasiswa Universitas Telkom Belajar Investasi Reksa Dana". Untuk selengkapnya kunjungi:

https://www.inews.id/finance/bisnis/mnc-sekuritas-dan-kb-valbury-am-gandeng-mahasiswa-universitas-te...

Publication

Having Fund with Mercu Buana University by MNC Securities & KB Valbury AM

30 October 2024Publication

Having Fund with Mercu Buana University by MNC Securities & KB Valbury AM

30 October 2024JAKARTA - MNC Sekuritas merupakan perusahaan sekuritas yang aktif dan konsisten dalam menggelar kegiatan edukasi pasar modal untuk menciptakan investor yang berkualitas. Salah satu bukti komitmen pengembangan investor pasar modal Tanah Air adalah konsistensi Perseroan dalam melakukan edukasi pasar modal, termasuk dalam rangka Bulan Inklusi Keuangan (BIK) dan Gerakan Nasional Cerdas Keuangan (GENCARKAN).

MNC Sekuritas bersama KB Valbury Asset Management memberikan edukasi reksa dana kepada lebih dari 100 mahasiswa Universitas Mercu Buana , Kampus Menteng pada Selasa (29/10/2024). Adapun materi edukasi disampaikan oleh General Manager KB Valbury Asset Management Dede Surjadi dan Head of Mutual Fund MNC Sekuritas Agustina Endah.

Dalam pemaparannya, General Manager KB Valbury Asset Management Dede Surjadi menjelaskan bahwa berinvestasi berbeda dengan menabung. Uang kehilangan nilainya seiring dengan berjalannya waktu karena dipengaruhi oleh inflasi. Untuk melawan inflasi maka perlu berinvestasi, khususnya investasi pada reksa dana yang dikelola oleh para profesional.

“Mulai disiplin menyisihkan uang untuk berinvestasi reksa dana, bahkan berinvestasi reksa dana bisa dengan harga yang terjangkau di aplikasi MotionTrade, dengan imbal hasil yang lumayan dan risiko yang terukur!” jelasnya.

Kepala Galeri Investasi Universitas Mercu Buana Menteng Riska Rosdiana dalam sambutannya menyampaikan terima kasih kepada MNC Sekuritas dan KB Valbury Asset Management. Menurutnya, acara ini adalah sarana agar mahasiswa dapat mengelola keuangan melalui reksa dana, yang tentunya sangat cocok untuk investor pemula.

"Selamat mengikuti seminar ini, saya mewakili jajaran Universitas Mercu Buana Menteng berharap acara ini dapat berjalan dengan lancar. Kami berharap seminar ini bisa memberikan inspirasi bagi mahasiswa untuk lebih aktif dalam berinvestasi pasar modal," ucap Riska.

Nikmati layanan investasi saham dan reksa dana dari #MNCSekuritas dengan segera unduh aplikasi MotionTrade dan jelajahi seamless experience. Aplikasi MotionTrade dapat diunduh di Google PlayStore dan Apple AppStore dengan link unduh onelink.to/motiontrade.

MNC Sekuritas, Invest with The Best!

---

Artikel ini telah diterbitkan di halaman SINDOnews.com pada Rabu, 30 Oktober 2024 - 11:10 WIB oleh Anto Kurniawan dengan judul "MNC Sekuritas dan KB Valbury AM Gelar Edukasi Reksa Dana di Universitas Mercu Buana". Untuk selengkapnya kunjungi:

https://ekbis.sindonews.com/read/1480639/178/mnc-sekuritas-dan-kb-valbury-am-gelar-edukasi-reksa-dan...

Publication

Having Fund with STIE Tri Bhakti by MNC Securities & KB Valbury AM

25 October 2024Publication

Having Fund with STIE Tri Bhakti by MNC Securities & KB Valbury AM

25 October 2024JAKARTA - MNC Sekuritas merupakan perusahaan sekuritas yang aktif dan konsisten dalam menggelar kegiatan edukasi pasar modal untuk menciptakan investor yang berkualitas. Salah satu bukti komitmen pengembangan investor pasar modal Tanah Air adalah konsistensi Perseroan dalam melakukan edukasi pasar modal, termasuk dalam rangka Bulan Inklusi Keuangan (BIK) dan Gerakan Nasional Cerdas Keuangan (GENCARKAN).

MNC Sekuritas dan KB Valbury Asset Management menggelar kegiatan edukasi reksa dana "Having Fund 2024" di STIE Tri Bhakti pada Kamis (24/10/2024). Materi edukasi disampaikan langsung oleh Direktur KB Valbury Asset Management Dede Surjadi dan Senior Marketing Mutual Fund MNC Sekuritas Wesly Andri. Antusiasme peserta terlihat dari ±150 mahasiswa yang turut hadir mengikuti kegiatan ini.

Direktur KB Valbury Asset Management, Dede Surjadi mengatakan, bahwa para mahasiswa dan juga para pekerja muda Indonesia perlu pemahaman yang tepat mengenai investasi di pasar modal Indonesia, khususnya investasi pada reksa dana.

“Melalui acara Having Fund 2024 ini, kami memaparkan pentingnya disiplin dan komitmen dalam berinvestasi dengan nilai yang masih terjangkau oleh para investor pemula. Kami memperkenalkan pula produk reksa dana yang cocok untuk tujuan tersebut, dimana produk tersebut dapat diperoleh melalui MotionTrade dari MNC Sekuritas,” ujar Dede.

Rektor STIE Tri Bhakti Drs.Widayatmoko, MM., M.Ikom dalam keterangan tertulisnya menerangkan, bahwa kolaborasi antara MNC Sekuritas dan STIE Tri Bhakti dilakukan untuk terus mengedukasi dan meningkatkan literasi pasar modal.

"Kami berharap agar mahasiswa lebih mengenal berbagai instrumen pasar modal, sehingga dapat membuka akses dan kesempatan mahasiswa untuk menjadi investor di pasar modal," tulis Widayatmoko.

Nikmati layanan investasi saham dan reksa dana dari #MNCSekuritas dengan segera unduh aplikasi MotionTrade dan jelajahi seamless experience. Aplikasi MotionTrade dapat diunduh di Google PlayStore dan Apple AppStore dengan link unduh onelink.to/motiontrade .

MNC Sekuritas, Invest with The Best!

---

Artikel ini telah diterbitkan di halaman SINDOnews.com pada Kamis, 24 Oktober 2024 - 16:27 WIB oleh Anto Kurniawan dengan judul "Mahasiswa STIE Tri Bhakti Antusias Ikuti Edukasi Having Fund oleh MNC Sekuritas & KB Valbury AM". Untuk selengkapnya kunjungi:

https://ekbis.sindonews.com/read/1477915/178/mahasiswa-stie-tri-bhakti-antusias-ikuti-edukasi-having....